Lumina Gold’s New PEA Shows 17M oz Gold Deposit Economic Today Yet Also Highly Leveraged to Gold Price with CEO Marshall Koval and VP Corp Development Scott Hicks

Lumina Gold Corp. was launched several years ago out of mining legend Ross Beaty’s (19.9% ownership) vision to develop a large gold deposit that could be monetized via a sale to a major gold producer during a gold upcycle. The company just released an updated PEA on its world-class, massive 17-million-ounce Cangrejos gold deposit in Ecuador. The PEA demonstrated 366k oz of gold production per year for 25 years with an AISC, net of copper, of only US$604/oz. The project now has a US$1.6 billion NPV5% at US$1,400/oz and US$2.5 billion NPV5% at US$1,680/oz. In this interview, President and CEO Marshall Koval and VP Corporate Development and Communications Scott Hicks discuss the results of the new PEA and how the company plans to move forward.

https://luminagold.com/ TSXV:LUM OTC:LMGDF

Lumina Gold Corp.’s presentation: https://luminagold.com/assets/docs/presentations/LumGLD_June-2020—Post-PEA-1591823752.pdf

Lumina’s PEA news release: https://www.miningstockeducation.com/2020/06/lumina-gold-announces-positive-cangrejos-preliminary-economic-assessment-us1-6-billion-npv-25-year-mine-life-and-production-of-more-360000-gold-ounces-per-year/

0:00 Introduction

1:35 How does 2020 PEA differ from 2018 PEA?

5:08 Feedback from Ross Beaty (19.9% ownership) on new PEA?

6:40 Viewing the new PEA through the eyes of a banker

7:51 Feasibility of raising US$1B to build the mine?

9:07 How does Lumina Gold differ from companies like Seabridge Gold, International Tower Hill Mines, NOVAGOLD, or Chesapeake Gold?

10:44 Since exit strategy is to sell Cangrejos to a major producer, what is the next step forward?

12:14 Have any majors signed confidentiality agreements?

13:14 What to expect in the next 6-12 months?

13:48 What would be an acceptable buyout price to Lumina Gold?

18:10 How much in the treasury now? Will you be financing soon?

19:00 Final thoughts

TRANSCRIPT:

Bill Powers: Thank you for tuning into Mining Stock Education again. I’m your host, Bill Powers. In today’s episode, we are going to be getting an update from Lumina Gold Corp. and their Cangrejos project there in Ecuador. A massive project. A worldwide top 15 gold development project. They’ve already demonstrated over 17 million gold ounces. Ross Beaty owns just under 20% of this company. There was a PEA done on this project in 2018, but the company just released an updated 2020 PEA, so I asked both Scott Hicks, the VP of Corporate Development, and Marshall Koval, the President and CEO to come on today’s show to give us an overview and an update.

So gentlemen, welcome back onto Mining Stock Education. Marshall, I’d like to kick it over to you first. Could you give us an overview of the 2020 PEA that you just put out, and what are some of the key differences versus the PEA that you put out two years ago?

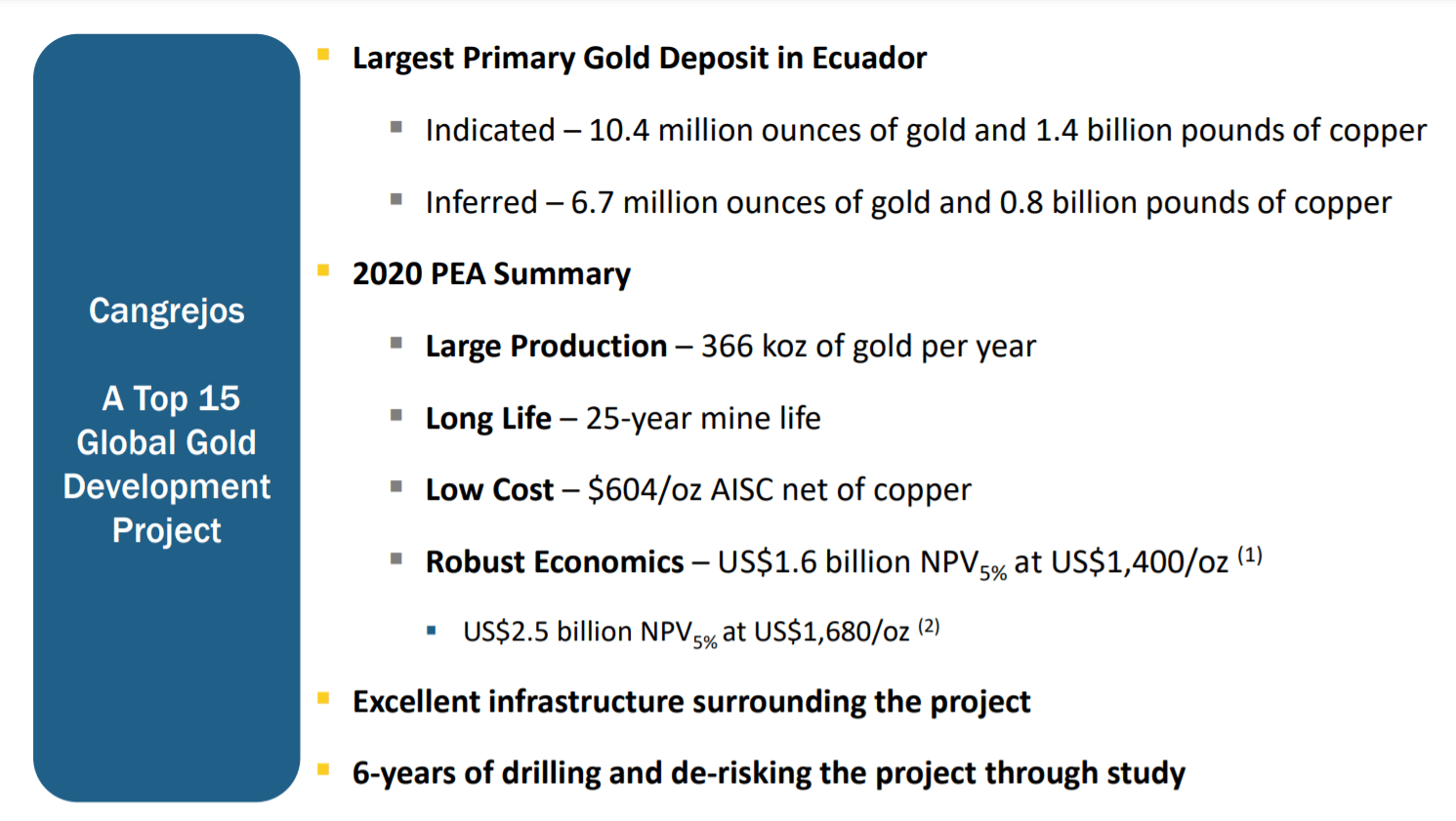

Marshall Koval: Hey Bill, thanks for having us today. Yeah, I think what we’ve demonstrated with this PEA that we just completed, is that obviously this is the largest gold deposit in Ecuador. It’s moving towards the development stage. We’ve had really good success with the work that we did between 2018 and today. We did quite a bit of drilling, about 40,000 meters. We advanced a lot of the engineering for the project. A lot of the project engineering is towards pre-feasibility study level. We’ve got to the point now where we understand the scale and the magnitude of the project with the addition of the Gran Bestia deposit.

So now we can really look at what is the infrastructure needs for the project? What is the economics look like at a PEA level? And really, if I kind of walk through a couple of the big issues and the big changes is, we designed the pit on this when we did the mine plan at $1,100/oz gold and about $2.35/lb copper. So the idea there was that we could have a defendable project that would survive multiple cycles in the gold price cycle. And we’ve achieved that by sort of a 25 year mine life.

We’ve also looked at optimization of the mining and the process plant to drive down operating costs as much as we can. Because when you look at the value proposition on an NPV basis, you’re going to be a lot more sensitive to operating costs and metal prices than you are the initial capital cost. So we went through, and the geometry of the mine, we started off with 40,000 tons per day. One of the questions we’ve heard before is, “How come you haven’t gone to a bigger initial throughput?” Because we plan to expand to 80,000 tons per day in year six. Well, a lot of that has to do with the mining geometry and the sinking rate and the ability to get to that production level straight off the bat.

So, some of the big improvements are a larger mining fleet. That helps drive down the operating costs. We looked at lower power consumers in the plant, like a high pressure grinding roll instead of a sag mill. A lot of those sorts of things went into this updated PEA. And again, we still have a low cost. We’re at about $604 gold AISC, net of copper, and really robust economics. It’s $1.6 billion NPV at a 5% discount rate at $1,400 gold.

There’s a lot of leverage. I mean, if you start to look at sort of 1,680 gold price, which is about 20% above the base case, you have a $2.5 billion NPV. So this thing has a lot of torque, and it has a lot of leverage to the gold price. And I think it really solidified this as a major project of kind of world-class scale. It’s the 37th largest project, regardless of mines, development projects in the world for gold. So we’re really excited about what we’ve been able to show here. And we look forward to continuing to move the project forward.

Bill: Marshall, when you were reviewing the results of this PEA… Before you published it, I’m sure you reviewed it with Ross Beaty. What was some of the feedback that Ross had?

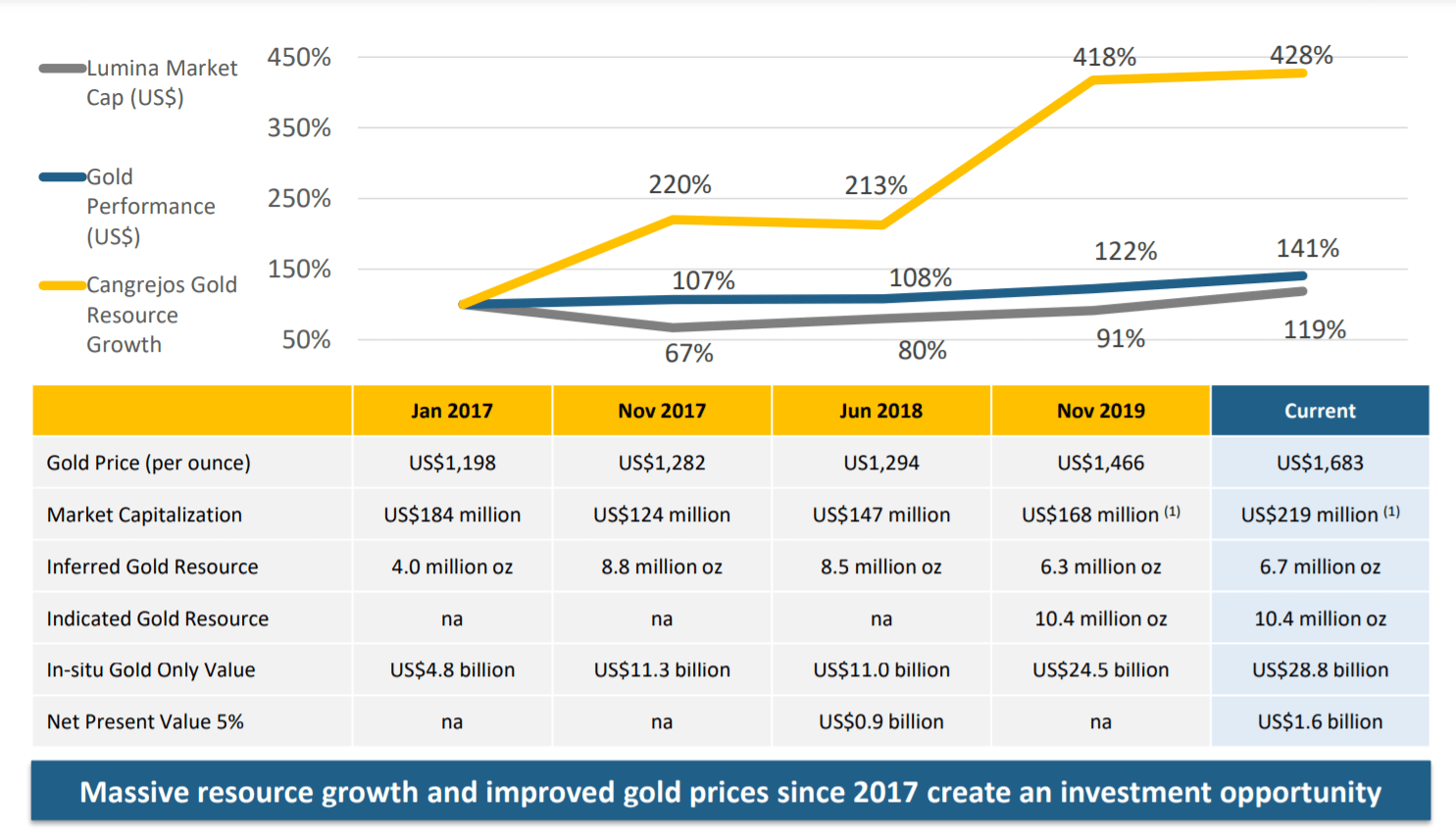

Marshall: He really likes where we’ve ended up, he likes some of the conservative estimates that we’ve put in as far as how we went about the project design. We have a good defendable project. And I think one of the frustrations that Ross has, as well as myself, if you go back, you can see this on our deck, on our website. But if you look at Lumina Gold from 2017 when we released our first resource estimate of 4 million ounces, and you move forward to the current scenario, so you sort of have our share prices moved up 19% over those three year period. Gold has moved up 41% over that same time period. And we’ve had a 400% plus increase in the resource at the project.

So we think there’s a disconnect in the market. We think that we’re severely undervalued, and that’s one of the frustrations that we’ve had as management, and we’ve delivered really good solid results here. I mean, this project will produce 366,000 ounces of gold per year, over 25 years. Not very many projects out there that have that ability. So those are kind of some of the comments. Ross was happy with what we achieved, but not so happy with the market.

Bill: Scott, your background, you come from the banking side. So as a banker, prior to working with the Lumina Group, when you look at this PEA through the eyes of a banker, what jumps out to you?

Scott: Thanks Bill. I mean, the most obvious things are obviously, as Marshall mentioned, the scale of the project really stands out for bigger companies to take a look at. And then, I think the other nice thing about this PEA is we’ve gone from a 16 year mine life to a 25 year mine life. And it’s so important in that obviously the mining industry is a very cyclical business. So it’s so important to have assets that allow you to hit multiple cycles. I mean, it’s one thing to model these things at a flat commodity price over 25 years, but we all know you’re going to have these big waves. So I think having that longer mine life is a big one.

And then, the other thing Marshall said, conservative estimates. And to expand on that, the mine planning for this was done $1,100 gold. So you’ve got a mine plan that can survive much lower gold prices than where we are now. And I think when an acquirer is looking at it, that’s really going to show through.

Bill: Your CapEx on this project is I believe US$1 billion. What is the realistic feasibility of something like that getting financed in this climate?

Scott: I think there is a lot of interesting options to finance that. I mean, you look at the cost of capitals from majors, it’s coming way down. Newmont’s doing bond deals these days the size of that CapEx around 3%. So very, very cheap cost of capital. So the big guys, I think it’s no problem. The intermediate guys, they obviously don’t have access to those types of bond markets. But I think we’re seeing the equity markets come back. This quarter’s been the strongest gold equity issuance markets in the last five years. So there’s the equity option.

We’re seeing banks come into Ecuador, Lundin Gold was able to get conventional bank debt as part of their financing in Ecuador. So that’s available. And then with this project, you’ve got the copper off-take side of it for the copper concentrate. Certainly you could bring in an Asian smelter partner for maybe 20-25% of the project CapEx. So I think there’s a lot of different avenues that somebody could pursue to put this project into production.

Bill: So as investors look at Lumina Gold now, they might compare it to other big deposits out there. We get our Chesapeake Gold, International Tower Hill, NOVAGOLD, Seabridge Gold, these type of projects, which investors typically tend to look at them as out-of-the-money call options on the price of gold. And many of their share prices have been doing good in the last six months to a year. How does Lumina Gold differ from these companies?

Scott: I think the biggest difference with some of these projects is, this is a project that works at… Our last study was at $1,300 gold. I think we demonstrated it had a robust NPV and IRR at $1,300 level. So it works at the lower gold prices. It’s large enough. It still gives you the torque, that those other projects have that you mentioned, but without maybe the huge CapEx associated with it. Some of those projects are $5-$6 billion builds.

And even in this much stronger gold price environment, I just don’t see companies rushing to build those types of very, very large projects right now. But we think $1 billion is achievable. And we’re very fortunate to be in an area of Ecuador with great infrastructure. We’re right next to the port, we’ve got power to site. And all of these things help with the reduced CapEx versus… To use an example, like Northern Dynasty, that has to build just so much infrastructure to make that project happen. Whereas we’re really fortunate to be surrounded with really good infrastructure.

Bill: As you look at moving this project forward, you’ve talked about, on this show and elsewhere, how the exit plan is to sell it to a major. And I remember when I had a conversation with Ross a couple of months ago, if I recall correctly, he said that there’s really no point in drilling out more ounces of gold once you reach that 25 year mine life, because you’re not going to get any value in terms of net present value currently. So, what would be the next logical steps to create the most shareholder value as you progress towards an eventual takeover?

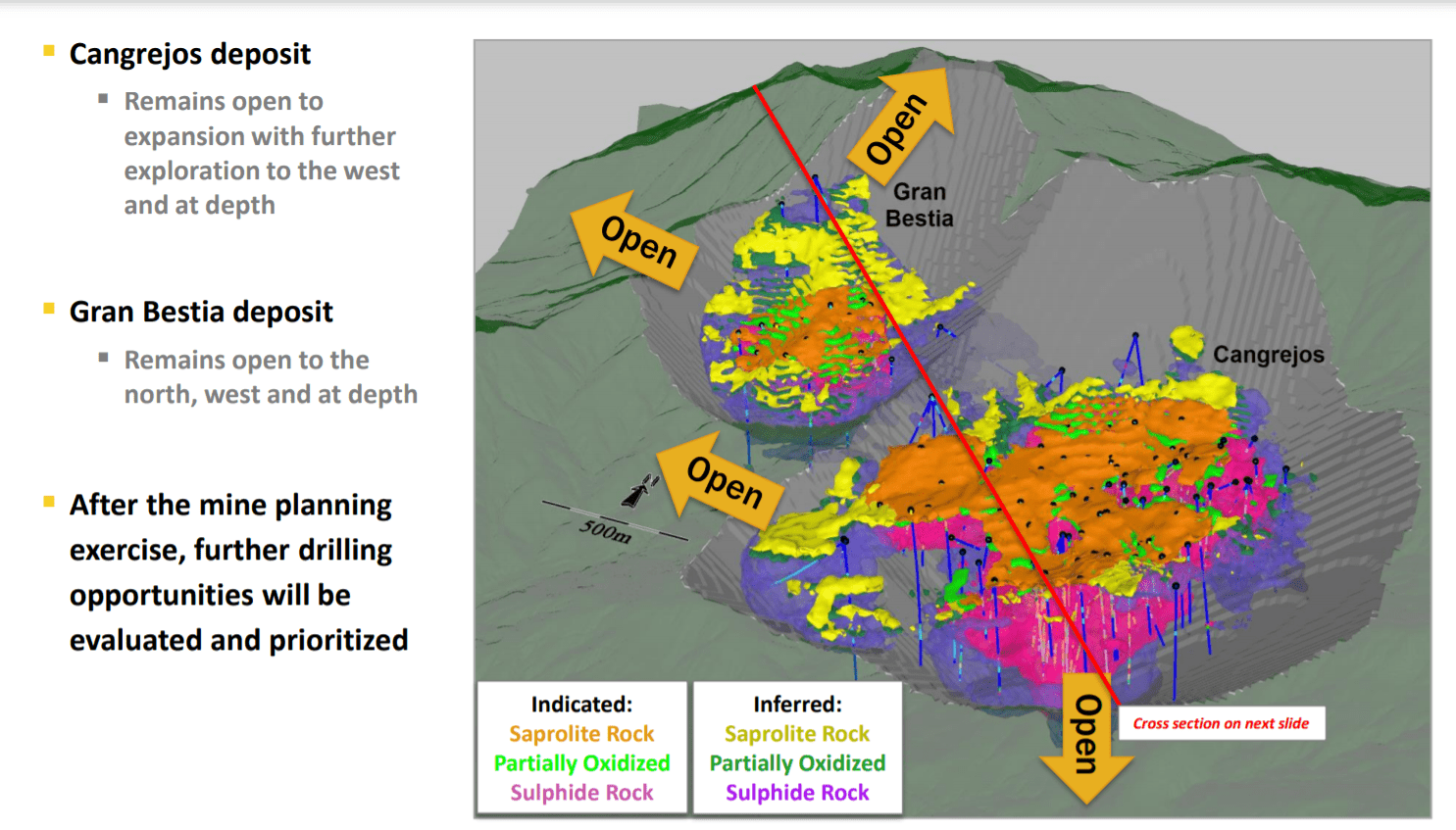

Marshall: I think even though the drilling aspect doesn’t add that much value, I want to just point out that the deposit, both Cangrejos and Gran Bestia is open in several areas so that you could add more potential ounces to it. But I think as far as your question goes in moving forward, what you really want to do is make sure you get this on the permitting path. And we’ve done substantial amount of work in the field with baseline studies. All your environmental baseline, archeological studies, hydro-geology, hydrology, ARD, water modeling, all this kind of stuff. Biodiversity studies. We’re setting up the project now so that it can move along that logical progression towards permitting, regardless of who would put this into production. So that’s going to be a key focus going forward. It’s not as sexy as putting out drill results, but it’s a critical aspect of the project that will continue to move forward.

Bill: Have any majors signed confidentiality agreements? Are you able to share at all about that?

Marshall: One of the things that we did is, before even entertained any inbound interest is we wanted to understand what Gran Bestia meant to the overall project. So in 2018, in the PEA we did, the Gran Bestia deposit was not part of that study. Subsequently we drilled it, and now we have a understanding for kind of the scale of Gran Bestia and what it means to the overall project design. Until we understood that metric to look at it internally and understand the value creation from Gran Bestia, as it contributes to the overall project, we hadn’t really talked to anybody. We needed to understand that. So we put out that updated resource last November, and we’ve had some inbound interest and we some CA’s in place. And that’s about all I can tell you at this point.

Bill: What more should investors expect over, let’s say, the next 6 to 12 months out of this project?

Marshall: Basically, I think what we’re going to see out of this PEA is we’re going to get recommendations out of the consultants. We already have a lot of those. We’re going to look at the sort of overall areas that you can optimize the project further. That’s going to be the permitting pathway, looking at some of the areas where you can do some engineering that may add value to it. And obviously any sort of exit that’s going to add the most value to the story.

Bill: Regarding the exit, I see in the chat rooms and online discussions, people talk about what would be an acceptable exit price. Obviously you’ve already articulated that you’re not fully satisfied with the valuation of the company now. When we see these buyouts, they’re done, a good one, maybe 50, 60% over the current market price. But it seems to me that that might not even be acceptable to you because you’re trading at US $188 million market cap as we speak. But the NPV you just put out as US$1.6 billion. So can you address potential takeover price? And would you accept shares or only cash?

Marshall: Yeah, well, shares and cash, those are the types of transactions that we’ve done before within the Lumina Group. So obviously that would be a scenario we would look at. Scott, I think you might talk about the developer peers in the Ecuador discount a little bit. And then also, maybe talk about some of the new coverage that we’ve got. Haywood put out a price target, and any sort of inputs there. Then I can kind of chime in along the way.

Scott: Kind of coming back to your question on premium, Bill. I mean, I think it’s important to remember that in the context of this scale of project, whether somebody is paying an extra 50, 100, $150 million worth of market cap, it’s not really going to move the needle on their perspective on the entire acquisition and the project. Just because it’s such a long life project, obviously the CapEx is a larger component of the build and getting it to production. So, that type of movement on the acquisition cost isn’t really going to be that huge of a deal from our perspective for a buyer.

If I think about kind of just value from the top down, you’ve got our $1.6 billion NPV at $1,400 gold, which, certainly that would be the long-term consensus view right now. You think about where developers might typically trade at. So call that a 0.5, 0.6 multiple. So you’re kind of sitting at around 800 million. We appreciate Ecuador’s a newer mining jurisdiction, so people are going to apply some sort of discount for that, whether it’s 10% or 20%.

I think if you think through all that, you can kind of see how you get to evaluation of something in and around that US$2 a share, just working down from our NPV and using some pretty reasonable assumptions. It’s going to be a question of getting a new, large gold participant to move into Ecuador. And, going to Marshall’s point there on the research coverage, Haywood put out a new target today based on the PEA. So they moved up from $1.50 price target to $1.80 Canadian price target. So I mean, that’s kind of where they expect that it could trade to in the market here just on a normal valuation. That’s not factoring in a takeover or anything. That’s their new price target. So those are just some benchmarks there for your listeners to think about.

Marshall: Yeah. And I think, Bill, the other thing to add there is we’re trading that CAD$0.76 today. And I think from that perspective, there’s a good investment thesis for savvy investors in the gold space that are looking at developers like ours. I think on the Ecuador discount point that Scott talks about, Fruta del Norte, being permitted, financed, and constructed, and now in operation, and the Mirador project, both these projects were… Fruta was about $700 million and Mirador was over a billion dollars. It shows that you can get international financing, you can permit, and you can construct and operate these projects in the country.

So part of that, as time goes on and more investment… You had Franklin Nevada come in and do a deal with SolGold on a royalty. And you had Newcrest come in and take out a stream on Fruta del Norte, and now they have 50%. Plus 50% of the free cash flow from Fruta. And as the market kind of matures, I think part of that discount will go away. So hopefully we would move more towards the Western world developers like Scott was talking about also.

Bill: You’ll need cash to move forward. So the question always comes from investors, what’s in the treasury? And are you going to need to finance anytime soon?

Scott: At the end of March, our last financials, we were sitting a shade over US$4 million in the treasury. Our burn rate’s going to go down quite significantly here, post finishing the PEA study. So, we think that we’ll run us out a good amount of time. Ross and the board are really of the view that they’d like to be anti-dilution focused. They don’t want to be raising at these undervalued levels. Ross has made it clear that he’s there to backstop the company, but doesn’t want to do an equity race. We don’t anticipate raising money in the near term here.

Bill: And that’s unique. I should point out for listeners that are newer to the Lumina Group. You don’t issue warrants, which is unique, on your financing. You have Ross owning one out of every five shares. Management and board owns 9.6% of the company. So between the management and the board and Ross, there’s 30% of the company right there. So you’re running the company, not just as employees, but as investors yourself. And I think that’s something important to point out. Gentlemen, do you have any further thoughts you’d like to share as we kind of wrap it up? What more would you like to leave with the investors listening to us?

Marshall: I think, take another look at the results of this PEA, and look at the group as a whole, and our history. I’ve been with Ross since 2004. And, I don’t know, we’ve managed to sell seven or eight companies through that period. One of the companies we have that I was the CEO of, Anfield Gold, we merged that into Equinox Gold.

We have a history of being able to create value in the market. Right now, when we look at the metrics that we put out from this PEA, and we see where our share price is trading, and knowing that we’re an exploration development company, not an operator. So we add value, de-risk, and we exit. I think there’s a really good value proposition here. We’re trading, like we’ve discussed here, below what we think we should be trading. And so we think there’s a lot of upside in the stock. So I would ask your audience and investors to take a hard look at us. Appreciate your time, Bill.

Bill: The website is LuminaGold.com. You can find it on the Venture Exchange in Toronto, under the ticker L-U-M. On the OTC in New York, you can look up L-M-G-D-F. The current share price in Canadian terms is 76 cents. It’s 50 cents in US dollars. And as I already mentioned, it’s about US$188 million market cap. Whereas the current PEA values the project at US$1.6 billion. Marshall and Scott, thanks for coming on today’s show and providing an update much appreciated.

Marshall: Thanks, Bill.

Scott: Thanks, Bill.