Blackrock Silver Announces Updated Preliminary Economic Assessment for Its Tonopah West Project in Nevada; +10 Year Mine Life Fortified by 90% Increase in Indicated Mineral Resources

Average production of 7.1 million ounces of AgEq per year at US$17.44/oz AgEq AISC underpins After-Tax IRR of 28% and US$437 million NPV on an initial capex of US$190 million at disciplined US$2,700/oz gold and US$31/oz silver operating case; economics scale to 79% IRR and US$1.55B NPV After-Tax at the 1-year analyst consensus forecast for gold and silver prices

Vancouver, British Columbia–(Newsfile Corp. – March 31, 2026) – Blackrock Silver Corp. (TSXV: BRC) (OTCQX: BKRRF) (FSE: AHZ0) (“Blackrock” or the “Company“) is pleased to announce the results of a Preliminary Economic Assessment (“PEA“) for its 100%-owned Tonopah West Project (“Tonopah West” or the “Project“), in one of the largest historic silver districts in North America, located on private land in Nye and Esmeralda counties, Nevada, United States, approximately 1 kilometer (km) west-northwest of Tonopah, Nevada. All dollar figures in this news release are in United States dollars unless otherwise noted.

The PEA was prepared by Minetech, LLC (“Minetech“) in accordance with Canadian Institute of Mining, Metallurgy and Petroleum (“CIM“) Definition Standards – For Mineral Resources and Mineral Reserves adopted May 19, 2014 (the “CIM Definition Standards“) and in accordance with National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101“) with an effective date of January 4, 2026.

The PEA is based on an updated mineral resource estimate prepared by RESPEC Company, LLC (“RESPEC“) in accordance with the CIM Definition Standards and NI 43-101 (the “MRE“). The effective date of the MRE is January 4, 2026.

Highlights of the Tonopah West PEA

(Ounces are troy; all tonnes metric)

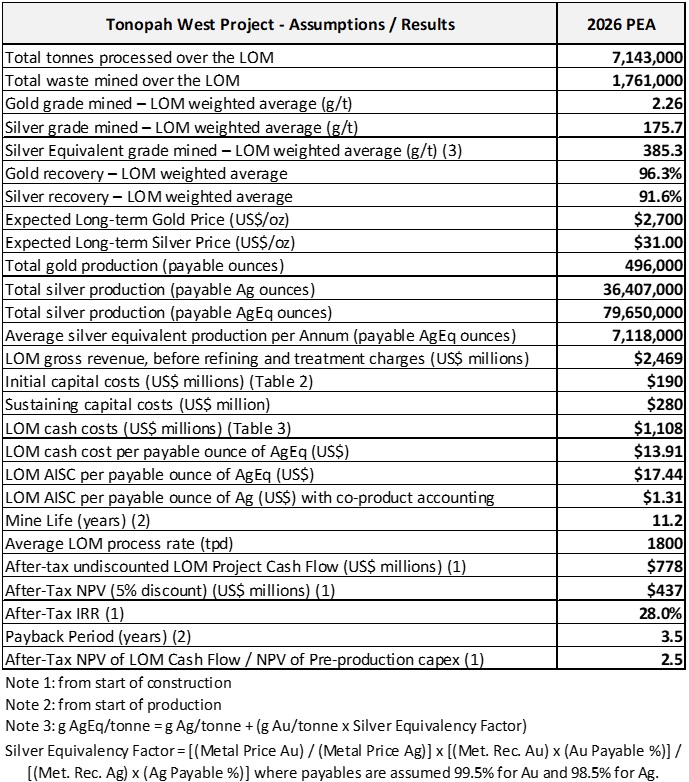

- Disciplined Base Case Economics: Secured with a conservative long-term silver (“Ag“) price of US$31 per ounce and a gold (“Au“) price of US$2,700 per ounce, the Project shows robust, after-tax net present value, discounted at 5% (“NPV5%“), of $437-million, and an after-tax internal rate of return (“IRR“) of 28% over an 11.2-year mine life (“LOM“) — ensuring operational resilience through a wide range of metal price cycles;

- Low Initial Capital: Calculated initial capital cost of US$190-million (including US$25-million contingency) with a base case payback period of 3.5 years;

- Increased Payable Metal: Enhanced mine plan delivers 89.6 million silver equivalent (“AgEq“) ounces, which equates to 79.6 million payable AgEq ounces — a 14% increase in payable silver and 17% increase in payable gold as compared to the previous preliminary economic assessment on Tonopah West dated effective September 4, 2024 (the “Original PEA“), with a US$778-million after-tax LOM cash flow.

- High-Margin, Low-Cost Operation: Anticipated All-In-Sustaining-Costs (“AISC“)1 of US$17.44 per silver equivalent ounce basis providing significant margin expansion potential;

- Increased Indicated AgEq Ounces: Improved indicated category mineral resource estimate comprising 2.75 million tonnes grading 454 grams per tonne (“g/t“) AgEq totaling 40.2 million ounces of AgEq (216.8 g/t Ag and 2.25 g/t Au for 19.2 million ounces of silver and 199,000 ounces of gold respectively) – a 90% increase over the previous mineral resource estimate on Tonopah West dated effective August 25, 2025 (the “Previous MRE“);

- Large Resource with Upside Potential: Increased inferred mineral resource with 5.54 million tonnes grading 466 g/t AgEq for 83 million ounces of silver equivalent (188.5 g/t Ag and 2.62 g/t Au totaling 33.6 million ounces of silver and 467,000 ounces of gold) in an inferred mineral resource category. The vein system is open to the east, northwest and at depth;

- Low-cost Geometry: Used a minimum mining width of three metres (3m), and Long Hole Stoping (cheaper costs) accounts for 88% of the tonnes mined while Cut and Fill mining accounts for 12% of the tonnes;

- Excellent Metallurgical Recoveries: Realized average recoveries of 91.6% for silver and 96.3% for gold from a 3-stage crushing circuit and processing plant;

- Exceptional Leverage to upside metal prices: Assessed at the 1-year analyst consensus forecast for gold and silver prices (US$66.90/oz Ag and US$4,554/oz Au), the Project delivers US$1.55B after-tax NPV5%, a 79% IRR, and a 1.4-year payback; and

- Unique location and infrastructure: Located on patented mineral claims (private land) adjacent to the town of Tonopah, Nevada, the Project benefits from its location, unprecedented infrastructure and profits from a stream-lined permitting process with only State and County agencies as stakeholders.

Andrew Pollard, Blackrock’s President & CEO, commented, “This updated PEA marks a significant milestone in the systematic de-risking of the Tonopah West Project. When we published our inaugural preliminary economic assessment 18-months ago, every ounce in the mine plan was inferred. Today we are presenting a high confidence Project underpinned by a substantial indicated resource base of 40.2 million silver equivalent ounces, nearly double what we reported in our Previous MRE. The increased confidence and expanded scale is evident with mine life extended 42% to 11.2 years; payable silver up 14%; payable gold improved by 17%, and after-tax NPV increased by 34% to US$437 million as compared to the Original PEA, which represents a 2.5 times return on initial capital of US$190 million. We have deliberately anchored this mine plan to a base case operating silver and gold price of US$31 and US$2,700 per ounce respectively, ensuring that Tonopah West is built for high-margin resilience across all price cycles. When framed against the current precious metal price environment, the economics of Tonopah West are standout. At the one-year analyst consensus forecast for silver price of US$66.90 per ounce and gold price of US$4,554 per ounce, the after-tax NPV shows US$1.55 billion, IRR climbs to 79%, and initial capital is returned in just 1.4 years. With permitting initiatives advancing in parallel, and an underground development decision targeted for H2-2027, management believes Tonopah West is one of the most compelling undeveloped silver assets in the Americas.”

A technical report prepared in accordance with NI 43-101 on the Project which includes the PEA and the MRE will be filed with the applicable Canadian securities regulators within 45 days of this news release. The technical report will be available under the Company’s profile on SEDAR+ (www.sedarplus.ca) and on the Company’s website (www.blackrocksilver.com). The results of the PEA are preliminary in nature and include inferred mineral resources that are considered too speculative geologically to have economic considerations applied to them to be classified as mineral reserves. There is no certainty that the results of the PEA will be realized. Mineral resources that are not mineral reserves do not have demonstrated economic viability.

Table 1: Key Economic Parameters of the PEA

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/676/290584_table1.jpg

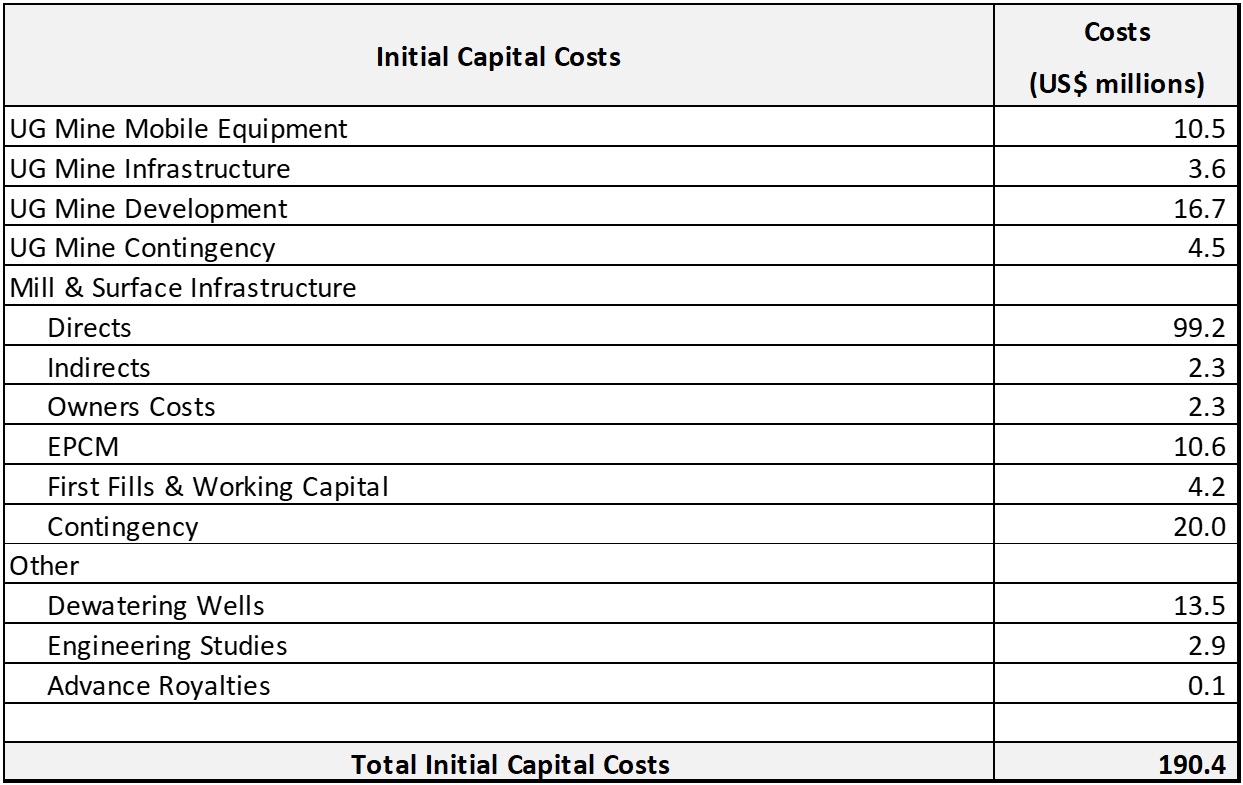

Capital Costs

The estimated capital costs to bring Tonopah West into operation are based on utilizing local and regional personnel and contractors. An underground development contractor will be employed to establish the portal, decline, underground drill platforms and pending successful results, initial mine development. As the mine develops, the Company will transition to owner mining. A geotechnical drill program was completed in 2025 along the decline corridor. The updated ground support, including shotcrete recommendations were incorporated in the capital expenditures. Contractors will construct all surface facilities including the process plant. After an initial ramp up period, mineralized material will be processed at a rate of 657,000 tonnes per year in a conventional three-stage crushing and milling plant including a refinery which will produce saleable gold and silver doré bars.

The initial capital expenditure is estimated at US$190.4 million for the construction period which includes US$24.5 million in contingency costs. An additional US$280 million is estimated for sustaining capital, principally associated with underground mining development, additional underground mobile equipment and infrastructure, delineation drilling and accrued reclamation expense over the LOM. The Company has included US$6.3 million for delineation access and drilling.

Capital cost estimates are based on industry standards and incorporate updated 4th quarter 2025 quotes and estimates from vendors.

A processing plant with a design capacity to treat 1,800 metric tonnes per day is planned with potential to easily expand to 2,000 tonnes per day. Extraction of gold and silver will be carried out by agitated cyanide leaching to produce a pregnant leach solution. The precious metal pregnant leach solution is separated from the solid material in counter-current decantation thickeners. Process tailings will be dewatered by pressure filtration. Solid tailings waste material from pressure filtration will be transported by dump truck to a lined dry-stack tailings storage area. For this evaluation, 20% of the tails were assumed to be used for backfill in the underground mine. Precious metal values will be recovered from the pregnant solution by Merrill-Crowe zinc precipitation, followed by precipitate smelting. Precipitate smelting will produce gold and silver doré bars.

Life-of-mine metal recovery averages 91.6% for silver and 96.3% for gold. All metallurgical testing and data analysis was completed at Kappes, Cassiday and Associates in Reno, Nevada.

Table 2: Capital Costs

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/676/290584_table2.jpg

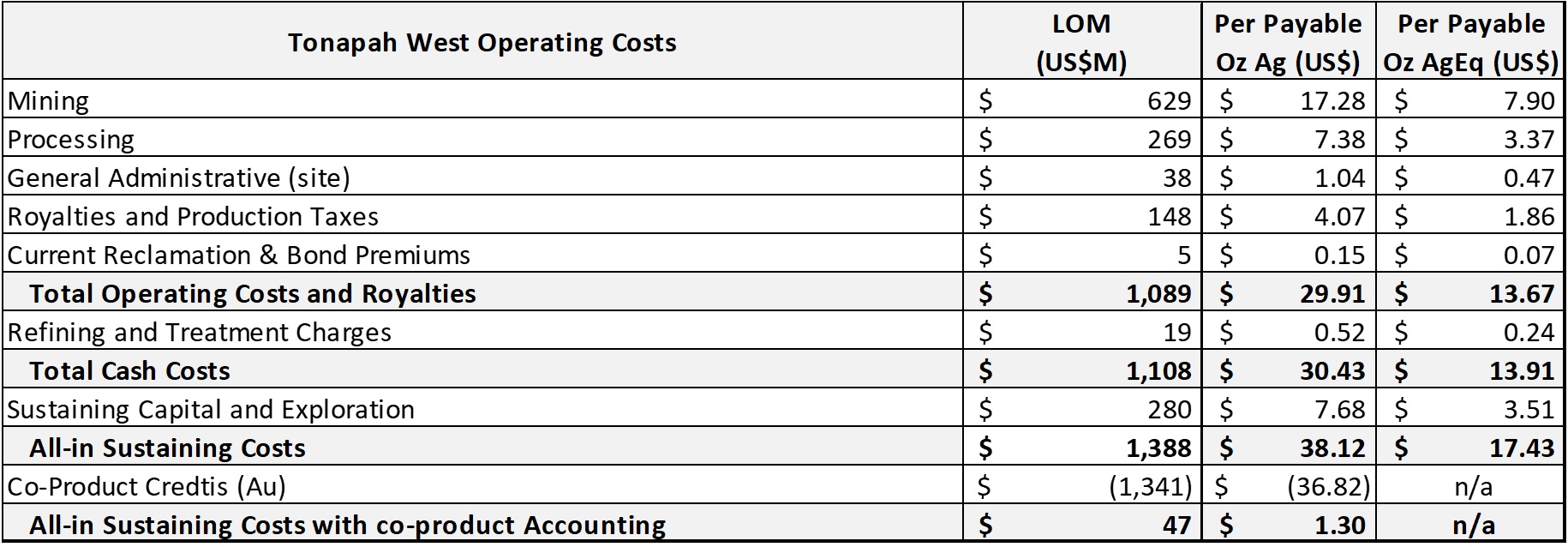

Operating Costs

The minable resource is accessed via a newly developed ramp system incorporating existing vertical shafts (rehabilitated) for ventilation and secondary escapeways. The minable resource will be extracted utilizing two mining methods, Sublevel Long Hole Stoping (“LH“) and Cut and Fill (“CF“) mining techniques. Cemented Rock Fill (“CRF“) and Hydraulic Fill are intended to be utilized as backfill. CRF media is sourced from the development waste rock, whereas Hydraulic Fill will be obtained from select tailings material. The minable resource will be transferred to surface via underground haul trucks. Mine operating, supplies and material costs were updated with vendor information 4th quarter of 2025.

The minimum mining width used in this PEA is three metres (3m), and the LH mining method accounts for 88% and CF mining accounts for 12%.

Process and general and administrative (G&A) costs have also been updated to reflect the increase in production rate and current material and supply costs.

Table 3: Operating Costs

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/676/290584_table3.jpg

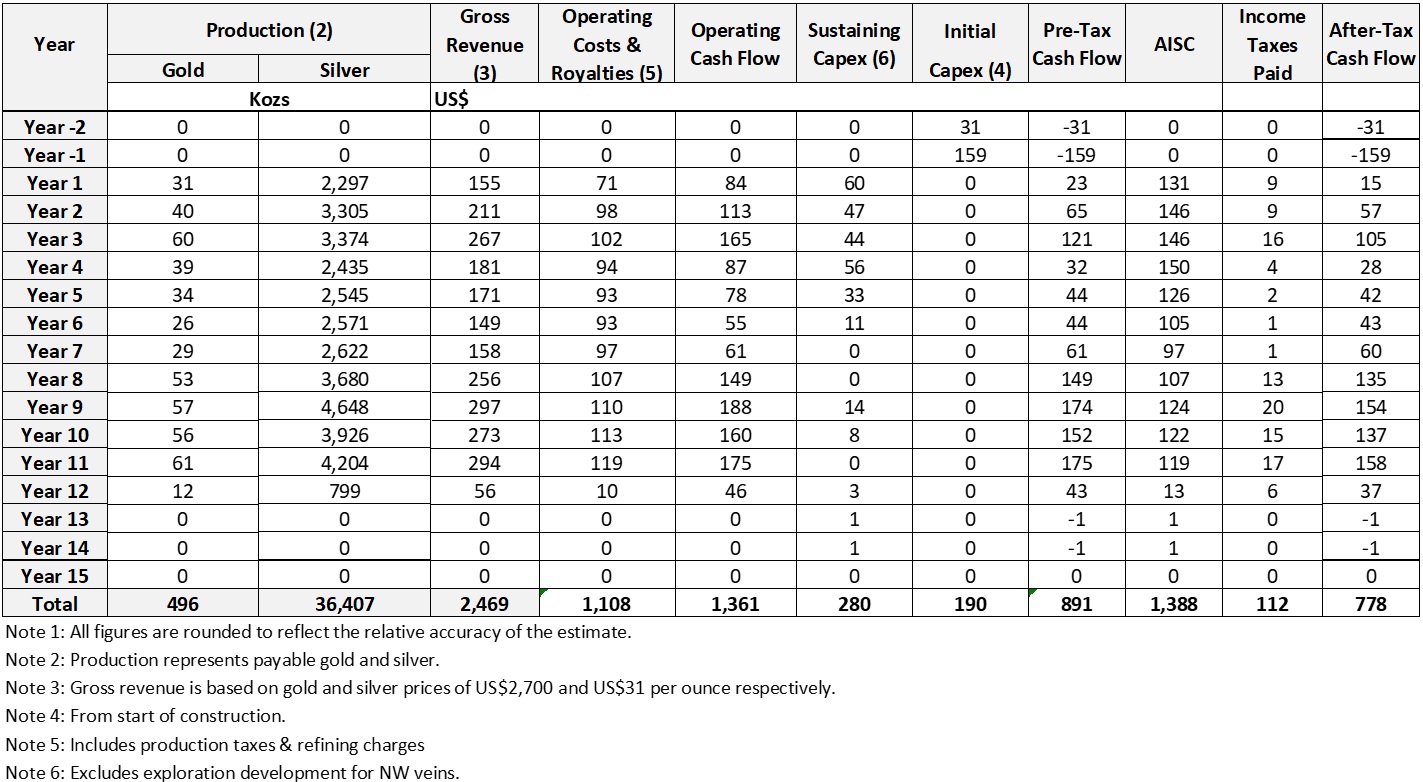

Table 4: LOM Operating and Financial Data

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/676/290584_table04.jpg

Table 5: Sensitivity Opex and Capex Variations

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/676/290584_table5.jpg

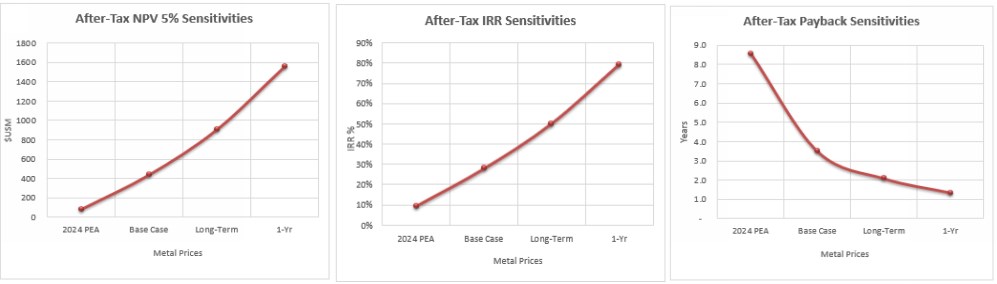

Figure 1: Sensitivity to Metal Prices – NPV, IRR and payback period

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/676/290584_d697e770447bba0c_006full.jpg

| Original PEA Metal Prices: | US$1,900/t-ounce Gold, | US$23.00/t-ounce Silver |

| Base Cash 2026 PEA Prices: | US$2,700/t-ounce Gold, | US$31.00/t-ounce Silver |

| Long-Term Metal Prices: | US$3,515/t-ounce Gold, | US$45.26/t-ounce Silver |

| 1-Year Metal Prices: | US$4,554/t-ounce Gold, | US$66.90/t-ounce Silver |

| Long-Term Metal Prices are average analyst consensus commodity price forecast as of March 3, 2026 | ||

| 1-Year Metal Prices are average analyst consensus commodity price forecast for 2027 as of March 3, 2026 | ||

Mineral Resource Estimate

The MRE was prepared by RESPEC in accordance with the CIM Definition Standards and NI 43-101. The effective date of the MRE is January 4, 2026.

Table 6: Tonopah West Indicated and Inferred Mineral Resource – Effective date January 4, 2026

| Cut-off Grade (AgEq g/t) (1) |

Tonnes (kt) | Grade | Contained Metal | Classification(4) | ||||

| Au (g/t) | Ag (g/t) | AgEq (g/t)(2) | Au (koz) | Ag (koz) | AgEq (koz)(3) | |||

| 140 | 2,750 | 2.25 | 216.8 | 454.3 | 199 | 19,167 | 40,159 | Indicated |

| 140 | 5,538 | 2.62 | 188.5 | 465.8 | 467 | 33,560 | 82,944 | Inferred |

1 AgEq cutoff grade is based on total mining, processing and G&A costs of US$128.6/tonne and a silver price of US$34/ounce.

2 For non-Victor areas, the AgEq grade ratio used is 108:1 based on silver and gold prices of US$35/ounce and US$3,500/ounce, respectively, and recoveries for silver and gold of 88% and 95%, respectively. For the Victor area, the Silver Equivalent grade ratio used is 102:1 based on silver and gold prices of US$35/ounce and US$3,500/ounce, respectively, and recoveries for silver and gold of 96% and 98%, respectively. AgEq Factor= (Ag Price / Au Price) x (Ag Rec / Au Rec); g AgEq/t = g Ag/t + (g Au/t / AgEq Factor).

3 Rounding as required by reporting guidelines may result in apparent discrepancies between tonnes, grade, and contained metal content.

4 Mineral resources are not mineral reserves and do not have demonstrated economic viability. There is no certainty that all or any part of the mineral resources estimated will be converted into mineral reserves. The quantity and grade of reported inferred mineral resources in this estimation are uncertain in nature and there has been insufficient exploration to define these inferred mineral resources as indicated mineral resources. It is uncertain if further exploration will result in upgrading them to the Indicated mineral resources category.

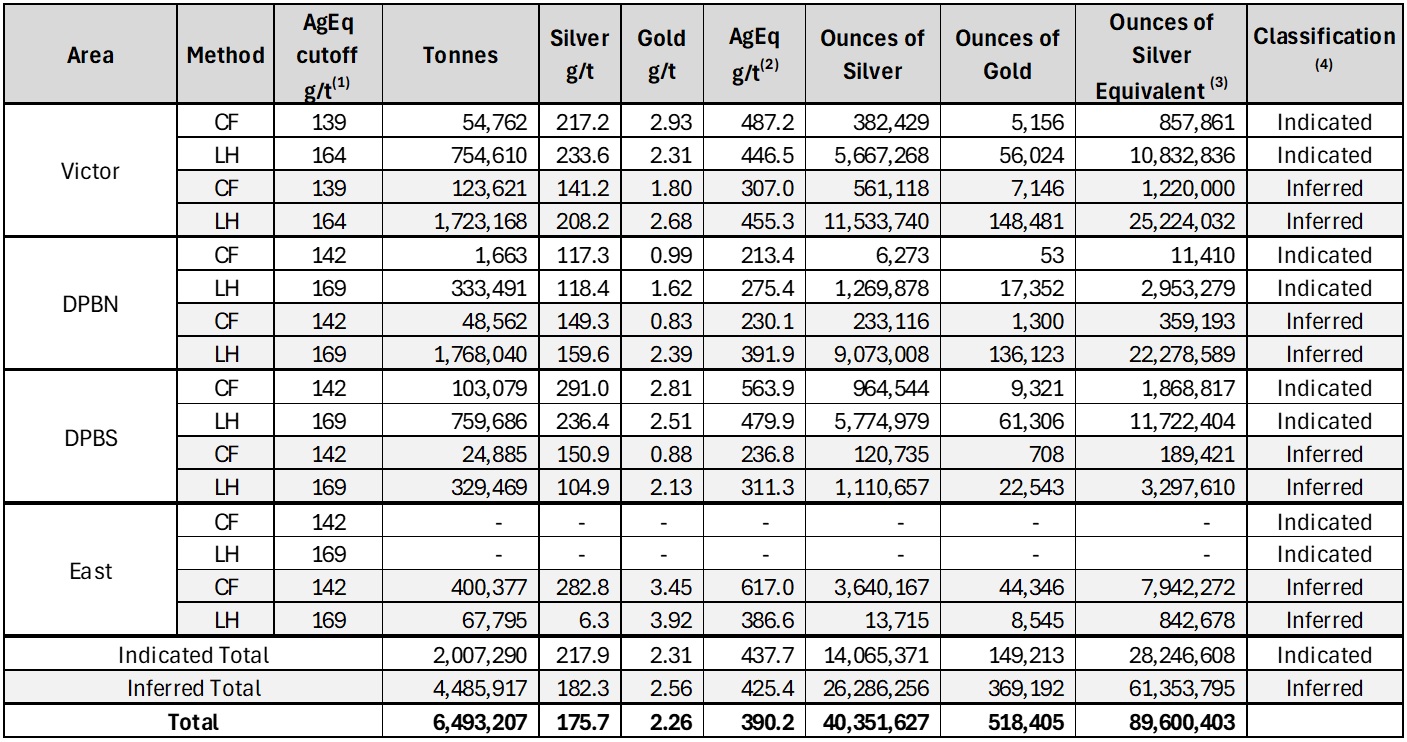

The MRE encompasses the spatial areas known as Victor, DPB North, DPB South, Northwest Step Out, and the East Extension areas. The Victor area is approximately 700-metres by 350-metres while the DPB area is 700-metres by 1,100-metres. NW Step Out represents a new extension of the vein zones to west-northwest. The East Extension is an area between the DPB South area and the eastern edge of the property. The spatial areas are not considered to be significantly different geologically but have been separated for logistical purposes in future mining scenarios. Table 7 presents the mineral resources subdivided by spatial area.

Table 7: Tonopah West Indicated and Inferred Mineral Resources by Area

| Area | AgEq cutoff g/t (1) |

Tonnes | Silver g/t |

Gold g/t |

AgEq g/t (2) |

Ounces of Silver |

Ounces of Gold |

Ounces of Silver Equivalent(3) |

Classification(4) |

| Victor | 140 | 882,000 | 255.2 | 2.65 | 525.2 | 7,241,000 | 75,000 | 14,899,000 | Indicated |

| 140 | 1,854,000 | 221.7 | 2.82 | 509.2 | 13,217,000 | 168,000 | 30,354,000 | Inferred | |

| DPB North | 140 | 263,000 | 146.1 | 1.79 | 339.4 | 1,233,000 | 15,000 | 2,865,000 | Indicated |

| 140 | 1,686,000 | 193.9 | 2.68 | 482.9 | 10,514,000 | 145,000 | 26,180,000 | Inferred | |

| DPB South | 140 | 1,281,000 | 213.3 | 2.12 | 442.0 | 8,787,000 | 87,000 | 18,209,000 | Indicated |

| 140 | 485,000 | 87.5 | 2.02 | 305.5 | 1,365,000 | 31,000 | 4,763,000 | Inferred | |

| NW Step Out | 140 | 323,000 | 183.4 | 2.03 | 402.8 | 1,907,000 | 21,000 | 4,186,000 | Indicated |

| 140 | 622,000 | 146.7 | 1.67 | 327.0 | 2,933,000 | 33,000 | 6,538,000 | Inferred | |

| East Extension |

140 | Indicated | |||||||

| 140 | 891,000 | 193.0 | 3.10 | 527.3 | 5,531,000 | 89,000 | 15,109,000 | Inferred | |

| TOTAL | 2,750,000 | 216.8 | 2.25 | 454.3 | 19,167,000 | 199,000 | 40,159,000 | Indicated | |

| 5,538,000 | 188.5 | 2.62 | 465.8 | 33,560,000 | 467,000 | 82,944,000 | Inferred | ||

1 AgEq cutoff grade is based on total mining, processing and G&A costs of US$128.6/tonne and a silver price of US$34/ounce.

2 For non-Victor areas a Silver Equivalent grade ratio used is 108:1 based on silver and gold prices of US$35/ounce and US$3,500/ounce, respectively, and recoveries for silver and gold of 88% and 95%, respectively. For the Victor area, Silver Equivalent grade ratio used is 102:1 based on silver and gold prices of US$35/ounce and US$3,500/ounce, respectively, and recoveries for silver and gold of 96% and 98%, respectively. AgEq Factor= (Ag Price / Au Price) x (Ag Rec / Au Rec); g AgEq/t = g Ag/t + (g Au/t / AgEq Factor).

3Rounding as required by reporting guidelines may result in apparent discrepancies between tonnes, grade, and contained metal content.

4 Mineral resources are not mineral reserves and do not have demonstrated economic viability. There is no certainty that all or any part of the mineral resources estimated will be converted into mineral reserves. The quantity and grade of reported Inferred mineral resources in this estimation are uncertain in nature and there has been insufficient exploration to define these Inferred mineral resources as Indicated mineral resources. It is uncertain if further exploration will result in upgrading them to the Indicated mineral resources category.

The NW Step Out area contains resources of 4.17 million AgEq ounces of Indicated and 6.54 million AgEq ounces in Inferred categories which are excluded from the PEA. There is significant exploration potential to expand this zone such that it could become big enough to be included in future mining studies.

To generate the MRE, RESPEC was supplied with geologic sections and levels by Blackrock. These geologic sections and levels were used to create a geological model which served as geological controls to construct three-dimensional grade domains to constrain the estimate. Silver and gold mineral resources were modelled and estimated as follows:

-

evaluate the drill data statistically;

-

create tightly constrained low-, medium- and high-grade mineral-domains using structural disks in Leapfrog software for both silver and gold on sets of cross sections spaced at 25-metre intervals;

-

use the mineral-domain structural disks as a basis to create three-dimensional wireframes in Leapfrog software;

-

code a block model to the silver and gold domains using the mineral-domain wireframes;

-

analyze the modelled mineralization geostatistically to aid in the establishment of estimation and classification parametres; and

-

interpolate grades into models comprised of 1.0(east-west) x 1.0(north-south) x 1.0(vertical)-meter blocks using the silver and gold mineral domains to explicitly constrain the grade estimations.

Drillhole assay samples were composited within the mineralized domains into 1.5-meter length composites. High-grade capping was completed on composite data and established using a statistical analysis for silver and gold. Silver was capped at 3,000 g/t, and gold was capped at 30 g/t. Specific gravity test work was completed for 374 core samples. Results indicate density can be subdivided by rock formation and mineral domain. Table 8 summarizes density values used in the block model.

Table 8: Tonopah West Density Summary

| Density Group | Density g/cm3 |

| non-mineralized group 1 (post-mineral volcanics) | 2.11 |

| non-mineralized group 2 | 2.41 |

| non-mineralized group 3 | 2.47 |

| mineralized 100 | 2.46 |

| mineralized 200 and 300 domains | 2.53 |

RESPEC utilized Inverse Distance Cubed (ID) interpolation for the estimation to obtain a localizing effect in the mid- and high-grade domains, and an Inverse Distance Squared (ID) in the low-grade domains where mineralization is more diffuse. All estimates are based on a block dimension of 1.0-meter by 1.0-meter by 1.0-meter blocks.

The original deposit has been depleted by historical mining in the Victor area. Approximately 200,000 tonnes of material were removed from the Victor resource estimate. In the DPB area, no historical mining records were documented.

A cut off for the reported mineral resource of 140 g/t AgEq was selected based an assumed mining costs for underground methods along with processing and G&A costs. At a 140 g/t AgEq cut off, the average grade of the indicated resource is 454.3 g/t AgEq and the average grade of the inferred resource is 465.8 g/t AgEq.

The MRE was prepared under the supervision of Mr. Jeffrey Bickel, CPG, an employee of RESPEC, and he has reviewed and approved the technical contents relating to the MRE in this news release.

Mr. Bickel has reviewed the sampling, assaying, and security procedures used at Tonopah West and it is his opinion that they follow industry standard procedures and are adequate for the estimation of the current MRE.

Mr. Bickel completed audits of the database, performed a site visit, and reviewed quality assurance and quality control data. After performing their review, he considers the assay data to be adequate for the estimation of the current MRE.

Mineral Resources Included in the Mine Plan

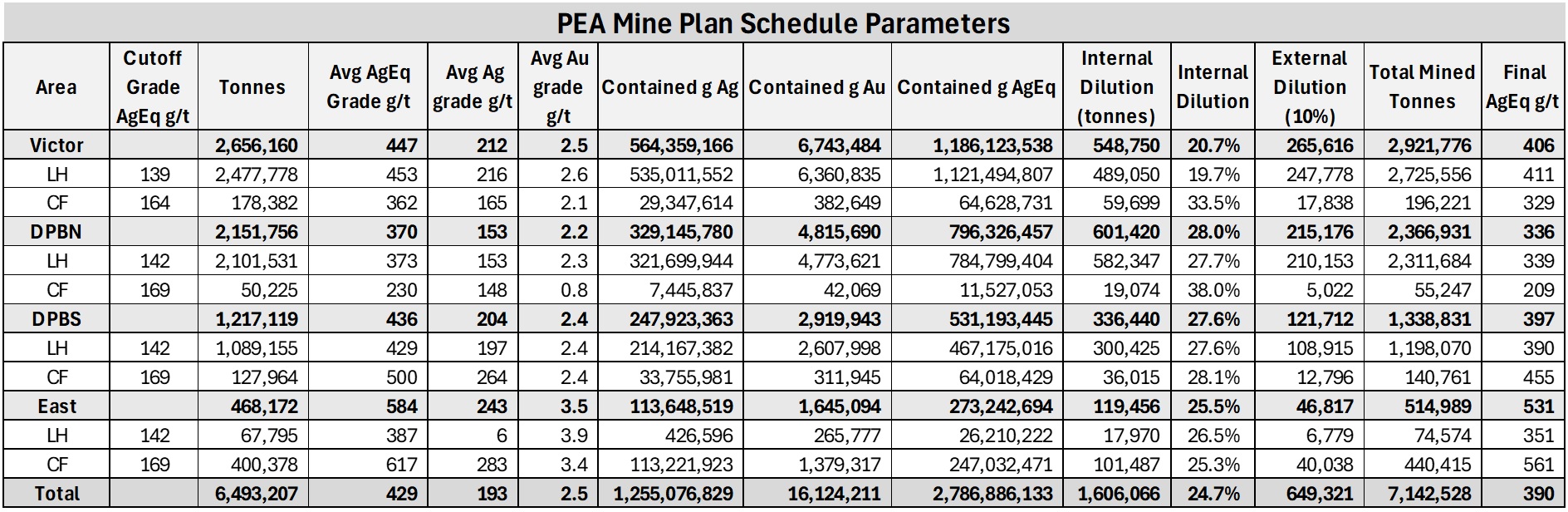

Maptek’s VulcanTM stope optimization software was used to produce an estimated mine plan based on the MRE. LH and CF were giving minimum mining dimensions the amount of sub-grade material that can be included in each stope excavation. Several runs were made and a maximum of 40% of allowable sub-grade material (internal dilution) allowed included in each shape showed the best tradeoff between bulk minable tonnages and grade. Sub-grade blocks may or may not carry grade. Actual internal dilution included in the mine plan ranges from 19.7% to 38% (Table 9). In addition to internal dilution an addition 10% of material at zero grade was added to account for external dilution e.g., wall rock and backfill.

Table 9: Tonopah West Mine Plan Resources

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/676/290584_table9.jpg

Total tonnes of 6,493,207 includes internal dilution of 1,606,066 tonnes

Table 10: Tonopah West Mine Plan Resources with Resource Classification (Undiluted)

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/676/290584_table10.jpg

1 AgEq cutoff grade is based on total mining, processing and G&A costs. Processing of non-Victor material US$41.16/tonne and Victor US$49.31/tonne including G & A. LH mining US$74.73/tonne and CF mining US$96.96 including G& A. Gold price of US$2,700 / troy oz and US$31.00 / troy ounce for silver less applicable recoveries, royalties, payable, shipping and sales charges.

2 Silver Equivalent is based on silver and gold prices of US$31.00/t-ounce and US$2700/t-ounce, respectively. These market values were reduced to contained realized values by deducting recovery, royalty, payable, shipping and sales charges. The realized contained values were US$27.74/t-ounce silver and US$2,552.36/t-ounce gold in the Victor; and US$25.37/t-ounce silver and US$2,474.18/t-ounce gold and US$25.37/t-ounce silver for non-Victor. AgEq = contained Silver grade + (Gold grade x realized Gold price / realized silver price.

3Rounding may result in apparent discrepancies between tonnes, grade, and contained metal content.

4 Mineral resources are not mineral reserves and do not have demonstrated economic viability. There is no certainty that all or any part of the mineral resources estimated will be converted into mineral reserves. The quantity and grade of reported Inferred mineral resources in this estimation are uncertain in nature and there has been insufficient exploration to define these Inferred mineral resources as Indicated mineral resources. It is uncertain if further exploration will result in upgrading them to the Indicated mineral resources category.

Reclamation and Closure Costs

Westland Engineering and Environmental Inc. estimates the bond required for reclamation and closure of the site at the end of the mine is US$9.2 million. The removal of processing equipment and general site grading is estimated at US$1.52 million and general reclamation costs are envisioned to be US$4.1 million.

If a surety bond with a 5% premium is acquired, the cost would be US$460,000 per annum which is captured in the cash flow model.

Qualified Persons

The “Qualified Persons” (as defined by NI 43-101) who were responsible for the PEA and MRE and who have verified and approved the contents of this news release are Robert H. Todd, P.E., of Minetech, Jeffery Bickel, C.P.G (AIPG) of RESPEC, Travis Manning, P.E., QP of Kappes, Cassiday & Associates, Thomas H. Bagan, P.E., MBA, SME-RM, an independent consulting mining engineer and Richard DeLong, QP of Westland Engineering and Environmental Inc.

Blackrock’s exploration activities at Tonopah West are conducted and supervised by Mr. William Howald, Executive Chairman of Blackrock. Mr. William Howald, AIPG Certified Professional Geologist #11041, is a Qualified Person as defined under NI 43-101 standards. He has reviewed and approved the contents of this news release.

The Qualified Persons referenced in this news release are not aware of any environmental, permitting, legal, title, taxation, socio-economic, marketing, political, or other relevant factors that could materially affect the PEA.

About Blackrock Silver Corp.

Blackrock Silver Corp. is an American-focused emerging primary silver developer systematically advancing the high-grade Tonopah West Project, situated in the historic “Queen of the Silver Camps” in a jurisdiction consistently ranked as one of the top mining regions globally. The Company is backstopped by a veteran board and technical team with a proven track record of discovering, financing, and building major precious metal mines in Nevada and globally. Blackrock is committed to establishing a secure, high-margin, domestic supply of silver and gold.

Additional information on Blackrock Silver Corp. can be found on its website at www.blackrocksilver.com and by reviewing its profile on SEDAR at www.sedarplus.ca.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Cautionary Note Regarding Forward-Looking Statements and Information

This news release contains “forward-looking statements” and “forward-looking information” (collectively, “forward-looking statements“) within the meaning of Canadian and United States securities legislation, including the United States Private Securities Litigation Reform Act of 1995. All statements, other than statements of historical fact, are forward-looking statements. Forward-looking statements in this news release relate to, among other things: the Company’s strategic plans; the results of the PEA; the economic potential and merits of the Project; the estimated amount and grade of mineral resources at the Project; precious metals prices; statements related to the operational resilience of Tonopah West; the PEA representing a viable development option for the Project; the timing and particulars of the development phases as identified in the PEA; estimates with respect to LOM, operating costs, sustaining capital costs, capex, AISC, cash costs, LOM production, mill throughput, NPV and after-tax IRR, payback period, production capacity and other metrics; the estimated economic returns from the Project; mining methods and extraction techniques; the advancement of permitting initiatives at the Project; an underground development decisions targeted for H2 2027; Project enhancement opportunities; the belief that Tonopah West is one of the most compelling undeveloped silver assets in the Amercias; and the timing of filing of a technical report in respect of the PEA and the MRE.

These forward-looking statements reflect the Company’s current views with respect to future events and are necessarily based upon a number of assumptions that, while considered reasonable by the Company, are inherently subject to significant operational, business, economic and regulatory uncertainties and contingencies. These assumptions include, among other things: conditions in general economic and financial markets; tonnage to be mined and processed; grades and recoveries; prices for silver and gold remaining as estimated; currency exchange rates remaining as estimated; reclamation estimates; reliability of the MRE and the assumptions upon which it is based; future operating costs; prices for energy inputs, labour, materials, supplies and services (including transportation); the availability of skilled labour and no labour related disruptions at any of the Company’s operations; no unplanned delays or interruptions in scheduled production; performance of available laboratory and other related services; availability of funds; all necessary permits, licenses and regulatory approvals for operations are received in a timely manner; the ability to secure and maintain title and ownership to properties and the surface rights necessary for operations; and the Company’s ability to comply with environmental, health and safety laws. The foregoing list of assumptions is not exhaustive.

The Company cautions the reader that forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause actual results and developments to differ materially from those expressed or implied by such forward-looking statements contained in this news release and the Company has made assumptions and estimates based on or related to many of these factors. Such factors include, without limitation: fluctuations in silver and gold prices; fluctuations in prices for energy inputs, labour, materials, supplies and services (including transportation); fluctuations in currency markets; operational risks and hazards inherent with the business of mining (including environmental accidents and hazards, industrial accidents, equipment breakdown, unusual or unexpected geological or structural formations, cave-ins, flooding and severe weather); risks relating to the credit worthiness or financial condition of suppliers, refiners and other parties with whom the Company does business; inadequate insurance, or inability to obtain insurance, to cover these risks and hazards; employee relations; relationships with, and claims by, local communities and indigenous populations; the ability to obtain all necessary permits, licenses and regulatory approvals in a timely manner; changes in laws, regulations and government practices in the jurisdictions where the Company operates; changes in national and local government, legislation, taxation, controls or regulations and political, legal or economic developments, including legal restrictions relating to mining and risks relating to expropriation; increased competition in the mining industry for equipment and qualified personnel; and those factors identified under the caption “Risks Factors” in the Company’s most recent Annual Information Form. Forward-looking statements are based on the expectations and opinions of the Company’s management on the date the statements are made. The assumptions used in the preparation of such statements, although considered reasonable at the time of preparation, may prove to be imprecise and, as such, readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date the statements were made. The Company undertakes no obligation to update or revise any forward-looking statements included in this news release if these beliefs, estimates and opinions or other circumstances should change, except as otherwise required by applicable law.

Cautionary Note for U.S. Investors Concerning Mineral Resources and Reserves

This news release has been prepared in accordance with the requirements of Canadian NI 43-101 and the CIM guidelines, which differ from the requirements of U.S. securities laws. NI 43-101 is a rule developed by the Canadian Securities Administrators that establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects. Canadian public disclosure standards, including NI 43-101, differ significantly from the requirements of the U.S. Securities and Exchange Commission (“SEC“), and information concerning mineralization, deposits, mineral reserve and mineral resource information contained or referred to herein may not be comparable to similar information disclosed by U.S. companies.

Non-IFRS Measures

The Company has included certain non-IFRS financial measures in this news release, such as sustaining capital costs, total cash costs and AISC which are not measures recognized under IFRS and do not have a standardized meaning prescribed by IFRS. As a result, these measures may not be comparable to similar measures reported by other companies. Each of these measures used are intended to provide additional information to the reader and should not be considered in isolation or as a substitute for measures prepared in accordance with IFRS. Non-IFRS financial measures used in this news release and common to the mining industry are defined below.

Sustaining Capital Costs

Sustaining capital costs are expenditures incurred during a production phase to sustain and maintain the existing assets so they can achieve constant expected levels of production from which the Company will derive economic benefits. Sustaining capital costs include expenditure for assets to retain their existing productive capacity as well as to enhance performance and reliability of the operations. Reclamation costs are accrued during the LOM and expended at the end of the mine life.

Total Cash Costs

Total cash costs are reflective of the cost of production. Total cash costs reported in the PEA include mining costs, processing, general and administrative costs of the mine, royalties and production taxes, reclamation and bond premiums and refining and treatment charges.

All-In Sustaining Costs (AISC)

Site-level all-in sustaining costs are reflective of all of the expenditures that are required to produce an ounce of silver from operations. All-in sustaining costs reported in the PEA include total cash costs, sustaining capital and exploration.

For Further Information, Contact:

Andrew Pollard

President and Chief Executive Officer

(604) 817-6044

[email protected]

Sean Thompson

Head of Investor Relations

1-800-380-1530

[email protected]

1 AISC is a non-IFRS financial performance measure with no standardized definition under International Financial Reporting Standards (IFRS). Please refer to “Non-IFRS Measures” at the end of this news release.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/290584