Why This Penny Stock Has Multi-Billion Dollar Potential with Trillion Energy CEO Art Halleran

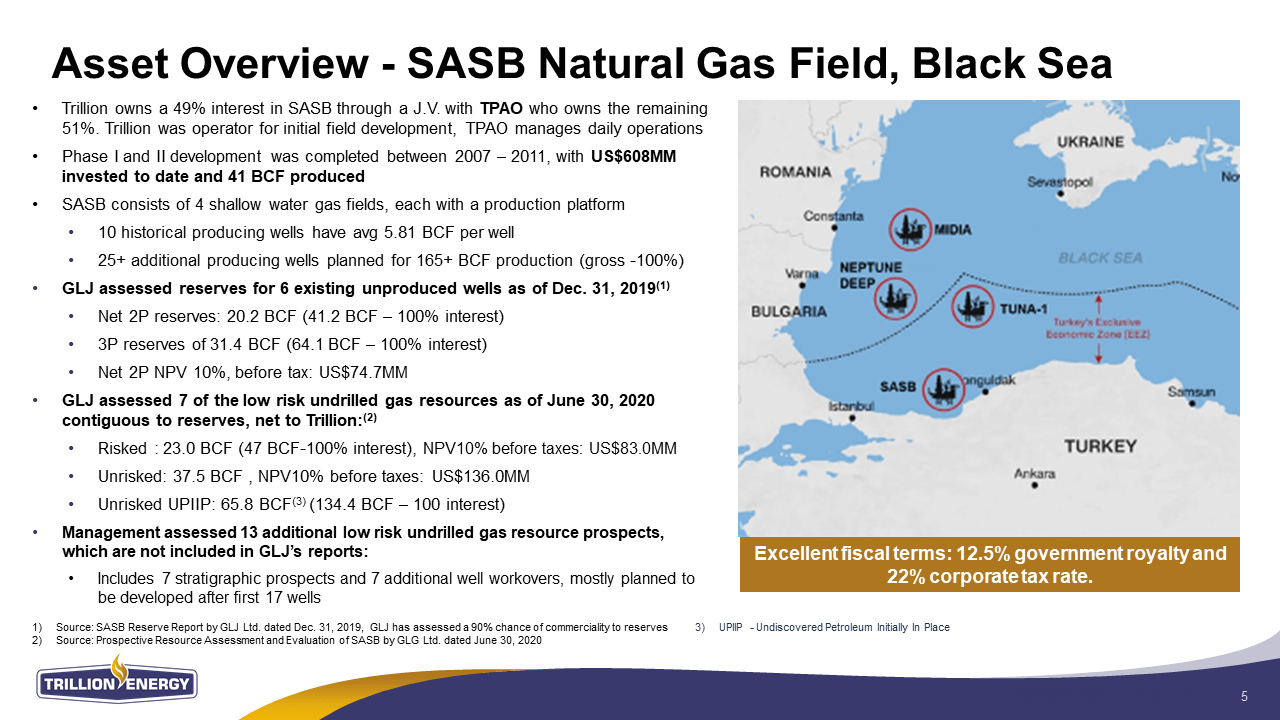

Trillion Energy (CSE:TCF – OTC:TCFF – FSX:3P2N) offers investors two genuine opportunities to create billions of dollars of market cap within two years explains CEO Art Halleran. Trillion is currently grossly undervalued with a market cap of only about US$20M while it owns infrastructure and gas reserves worth hundreds of millions of dollars. Furthermore, the company expects to be cash-flowing US$4M+/month in just 18 months from now. But over the next 1-2 years Trillion will be pursuing massive returns for its investors through exploration programs at its 49% owned SASB gas project in the Black Sea just off the cost of Turkey and at its 100% owned license of 42,833 hectares oil exploration block in southern Turkey which covers the northern extension of the prolific Iraq/Zagros Basin.

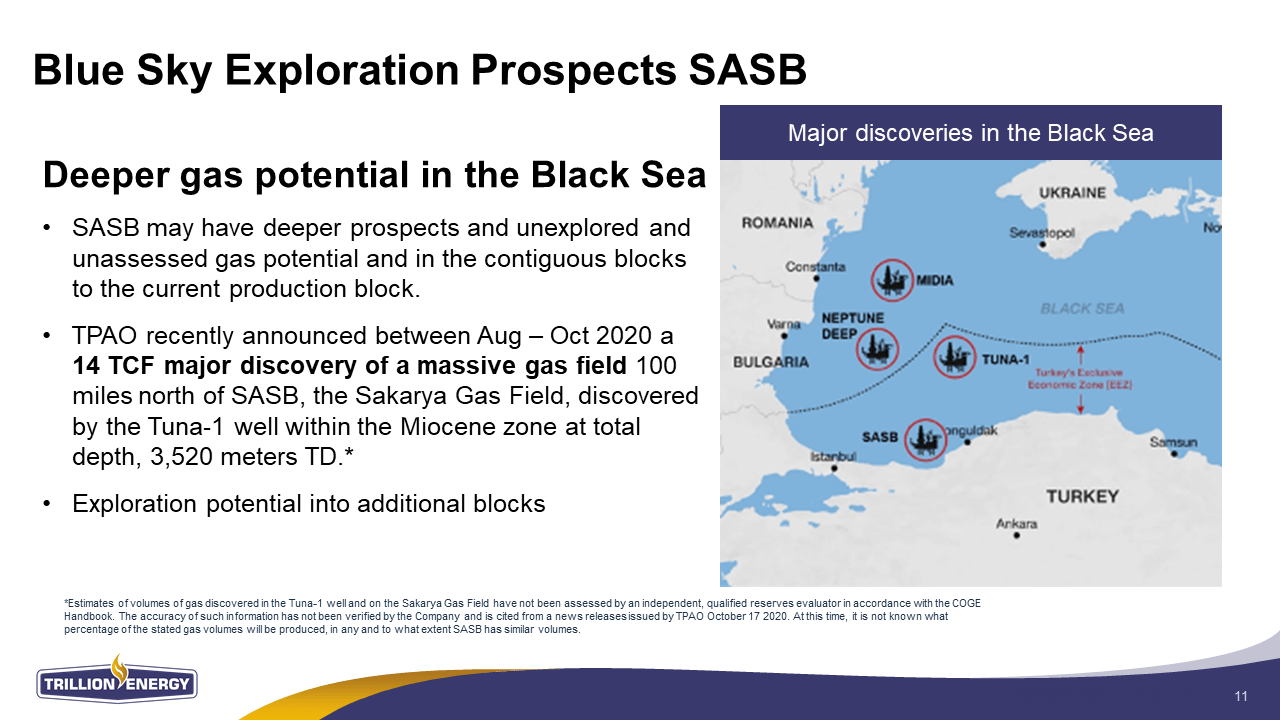

Trillion Energy’s SASB gas field is located just 100km south of the largest gas discovery in 30 years in Europe (14 TCF) and is the only nearology play in the region. Art has said that only a 1 TCF discovery would move Trillion from a penny stock to a $10+ stock quickly. Art stated, “so on our [license] block, we’re going to be looking for deeper potential because we have the same source rocks [as the 14 TCF discovery]. And the idea is we have to look for the reservoir rocks, but at the same time now, we are going to apply for a technical evaluation permit for maybe a hundred thousand hectares. And what that does is gives us the ability to take a large piece of land around a block and do geological studies to evaluate for similar type prospects that we have on our block, but also for deeper and different type of deposits that potentially could be a lot larger.”

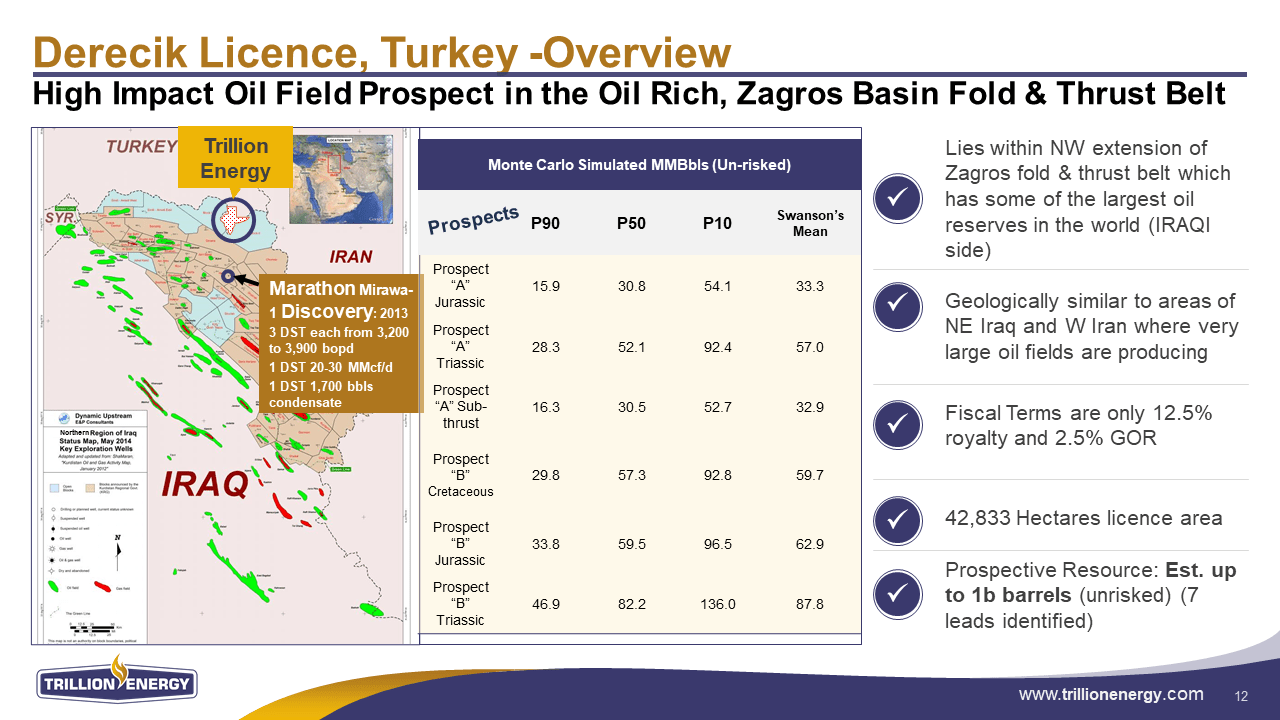

Trillion Energy will also be drilling next year its oil exploration license in southern Turkey in pursuit of a billion-plus dollar payday. Art pointed out that because they are in Turkey not Iraq they are in a safe location and their cost of drilling is about 1/6 the cost south of the border. Yet Trillion benefits from the same geology that has produced billions of dollars of oil wealth south of the border: “We have the same geology. We have the same reservoirs, the same source rocks. We have oil seeps that the oil has been tested, which is identical to the oil that’s produced in northern Iraq. And we have a location there that’s defined by seismic. We own it one hundred percent. We have a large landholding and we are drill-ready. And it’s an exploration location and if we hit even a small field compared to what we see south of the border, our shares are multiples of $10 value, right? Because you’re talking fifty million barrels recoverable, a hundred million barrels recoverable. With a hundred million barrels we’ll have a market cap value of basically $4 to $5 billion.”

TRANSCRIPT:

Bill Powers: Thank you for tuning into Mining Stock Education. I’m your host, Bill Powers. And in today’s show, we are doing a follow-up interview with CEO Art Halleran of Trillion Energy. We featured this company about two weeks ago and there was a nice, about 200% run in the stock. It’s experienced the pullback since then. There’ve been questions that have come in, both from listeners, as well as some of my friends that are texting me, “Bill, are you going to sell? What are you going to do? Is there still potential here?” And my answer was I haven’t sold anything. And let me explain to you why I think that there’s not just a little potential, but potentially huge potential that we’re going to discuss today. And I learned about this, not just the undervalued nature of the company, but the massive, even multi-billion dollar market cap potential, in my first call, which was about an hour with Art Halleran.

And we didn’t cover that in the introductory interview because there’s only so much you can cover, but we’re going to delve into it a little bit more. We’ve covered the undervalued nature of the company. If you look at the market cap, it’s about US$20 million, but if you were to build the infrastructure that they have today for their natural gas production in the Black Sea off the coast of Turkey, it’d probably cost you close to a half a billion dollars, their cost (as 49% owner). And then on an intrinsic value, if you look at the gas reserves they are over a dollar per share, yet the shares are trading between 15 and 20 cents U.S. right now.

The undervalued story is there, it’s still there, but the growth and the huge blue sky potential is what we’re going to delve into more today. So, Art welcome back onto the program and for the first question it is regarding your compensation and skin in the game. Some questions came back wanting to know about his. I believe you have about 6 million shares or so. And the question was if the company is so undervalued, why didn’t you buy more than only 6 million shares? If we could start there, please.

Art Halleran: Okay. Well, thanks for the second interview. I believed that an investor puts his money into the company waiting for the success. And also as a CEO, I believe the same thing. And if I don’t believe in myself, how can I get other people to believe in my story? So the reason why I have 6 million shares is that I initially was an independent director before I took the company over. And so when I became the CEO, I didn’t have very many shares, but at the same time, I only charge a minimum wage when I started, because I thought, why draw $25,000 a month from the start, if I’m still working at it, why should I get paid and the investors don’t? So I charged between eight to 10 grand a month. And that’s the wage that I get.

My wage will increase to 13 grand a month. Once I drilled the first well on the SASB. And then it goes to 25 grand a month when the first phase or undeveloped discoveries are on production. I get paid the same for my successes as the shareholders do. Getting back to the why at 6 million shares, I converted 90% of my wages into the shares. I paid invoices and put money into the company. I converted that to the shares. And so when you only make 8 to 10 grand a month and you convert into shares, it’s a slow build. Whereas I could have said, I’m going to pay $25,000 a month because I have 40 years experience. I have a PhD for the last three and a half years I got 25 grand a month, I can convert it all to shares, and I would have a zillion shares, which would not be fair to the shareholder because my payday is their payday.

Bill: And Art at that time, we should also point out that you used your own money. When you said you converted invoices into shares, you use your own money for some of those initial studies to help move the project forward, right?

Art: That’s correct. For key studies that we needed for the engineering report, we couldn’t raise the cash. So if I didn’t use my money, we’d probably still in that position right now. I use my money to pay for some of the seismic reprocessing and remapping so that we would have that data for the engineering report. And when you look at the engineering report, that added a couple of hundred million dollar value and it’s just because it’s a report, but it’s credible third-party whereas before us just saying it has no credibility.

Bill: Art, the second question that came in was how can this be so undervalued? And part of that goes to how you acquired the SASB project and how it’s not reflected on your books. Could you give us a brief, succinct answer for this please?

Art: Yeah, so we purchased a $300 million asset or about $2.7 million. This was the sub-co, but because there was virtually no reserves left in SASB and there was no value really attached to it, we were given advice by auditors and also people who knew a lot about the security laws and so on. They said, we have no reserves because remember we didn’t have that report. We have no reserves then we have to write off on the assets. And now the fact that we have the reserves back on, we are now looking at getting legal advice, putting that asset back on the books, the comment was you can’t have a couple of hundred million dollar asset if you have no reserves attached to it. Whereas now we do have the reserves attached to it.

Bill: The reserves you factor into your intrinsic value that you’ve shared is over a dollar per share U.S. and this is at the SASB project. You told me you viewed this project as the engine of the company, as in September of this year, if all goes as planned, you’re going to be starting to receive $1 million plus cash flow per month. But we didn’t delve into in our last interview, the growth potential that you see here, talk to us about in 18 months, what type of cashflow are we looking at?

Art: In our initial talk, I was talking about the actual drilled, not produced pools. So we have four of those. And so all our numbers are $1.4 to $1.8 million cash flow per month comes from those ones, but we have another six developmental locations that will be equivalent to those four. You can’t say you’re a hundred percent there because they were not tested and drilled, but they’re identical and we have an 80% success rate. We’ll continue drilling those and those will be added on. And so we should be up to four million dollars per month cash flow. And also another thing that came up is that we will… Actually three of the locations we will end up doing first. And those three locations alone will generate up to $1.4 million a month cashflow. But over 24 months, it’s an average of a million dollars a month, just from those three actions.

Bill: There’s growth that you see as a PhD geologist of four decades of doing this. Talk a little bit more about the blue sky growth that you can see that may not be reflected on paper yet.

Art: When you have an engineering report, there’s a lot of, I call paper cutting. If you just take the regular engineer report that we have proven, developed locations that we haven’t produced and also the prospects, it’s gives us a net value of about US$157 million. But in that they penalized 10% by saying, if we don’t get the money. And at the same time, they use very pessimistic recovery factors of as low as 56% recovery. That means of the hundred percent gas that we have mapped. We only recover 56%, but we already have experience from the four fields. So we know what it’s going to do. So just changing those two numbers for a 2P type reserve and so on, we’ve already upped it to $230 million. From $157 to $230 million by spending no more money just by putting the correct recovery factors in it and removing a penalty that shouldn’t exist because we get the money penalty isn’t there, right?

And then the high side, it’s up to $400 million. That’s our percent that is just using their reports and changing a few of the paper numbers. Right. We also have exploration that we have on the block and some of the risk factors they use for the development locations, or… I won’t get into it. But once we start correcting that and the exploration locations we’re going to de-risk because we’re going to start redoing the seismic again, middle of the road to 2P conservative gives us the value of over $400 million. And the high end is up to $800 million. And that is just from the targets that we have identified. A lot of that add is just paper adds and exploration is redo the seismic because it was good quality seismic, but it was a reprocess with older methods. We have new methods now, and then we can de-risk a lot of the exploration. So that is what we know existed between US$400-$800 million (NPV10).

Bill: Intrinsic value then, what would that translate into approximately on a per share basis?

Art: It would be about, I think it was 4 to 5 bucks. Because if the value is about a dollar, a dollar 25 or 156 million, 400 million, you could say three times up, four times up, 400 to 800 million.

Bill: Art in this past week, I scheduled a call with one of your key shareholders. And I just wanted to know why they invested in your company and understand from their perspective, the blue sky potential. This key shareholder owns millions of shares. And he’s been invested in Trillion since 2015. And his average cost basis is actually higher than where the shares are trading at today. And I said, “okay so tell me why you’re still holding onto your shares. Let’s start with the SASB.” And I was using a five to six, multiple times your cashflow to try to calculate an approximate market cap of where you might go. In his perspective he said, “Bill, I’m hoping for a 15 times multiple because with energy stocks, if you can show the blue sky potential, the market often rewards you with a 15 times multiple.” That was music to my ears.

The second thing he said is because we’re only 80 kilometers South of the biggest natural gas discovery of 14 TCF, natural gas discovery in Europe, the biggest one in 30 years, he says, “I’m expecting and hoping for somewhere between a 1 to 3 TCF, natural gas discovery.” Because he said anything above a one is world-class. Okay, assuming he’s. Right. And you discover something one TCF, this is the blue sky. What does that translate into on a per share basis?

Art: It’ll be at least 10 bucks.

Bill: 10 bucks in addition to what the value already is in the company?

Art: Yeah. And you can see if I say five to six and he says 15, shows you I’m a pessimistic guy.

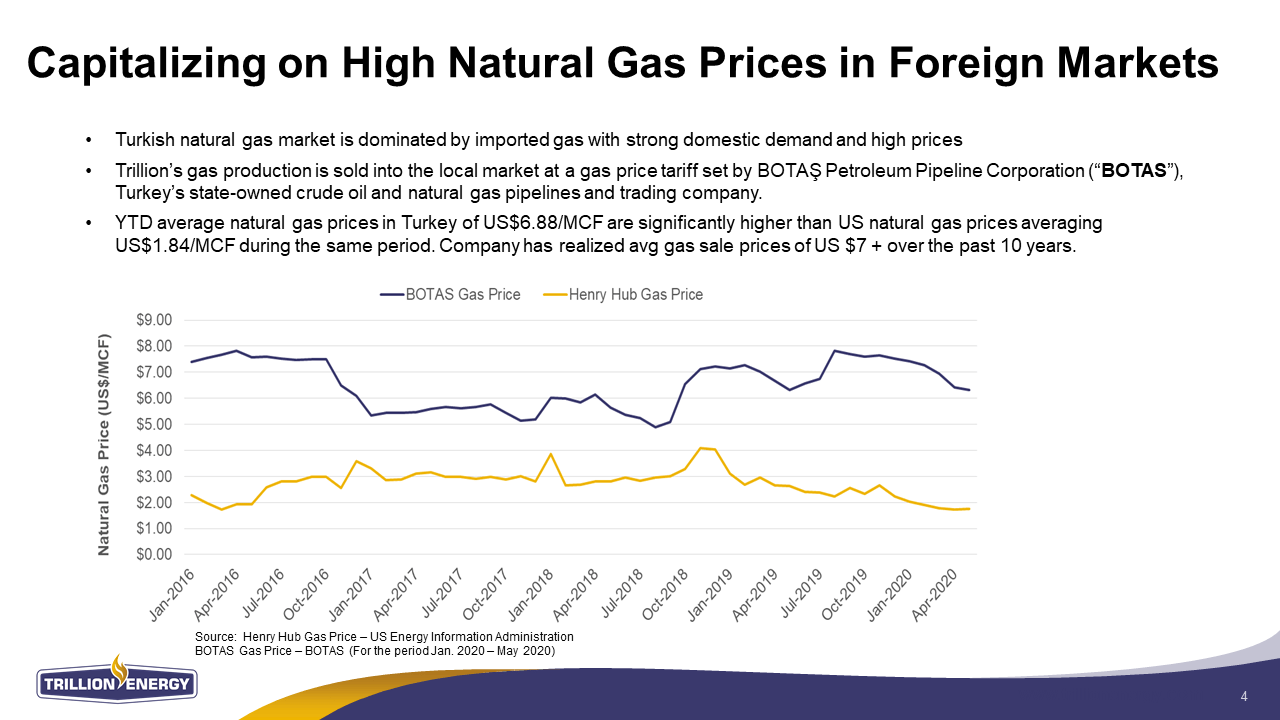

Bill: Last thing, before we leave the SASB gas field, your production is about $2.35 per MCF, right. But you’re going to be paid. You expect about $7 per MCF, which is multiples of what North American gas producers get.

Art: Yeah, that’s correct. And like I said, there was a crunch for the [inaudible 00:15:36] but every month. January, February, and March, we have received a price increase in our gas in Turkey. And we project that the trend will continue. And when you talk about the large discovery at the 80 kilometers North of us. With our seismic, and there was some 2D seismic lines. And so on our block, we’re going to be looking for a deeper potential because we have the same source rocks. And the idea is we have to look for the reservoir rocks, but at the same time now, we are going to apply for a technical evaluation permit and maybe a hundred thousand hectares. And what that does is give us the ability to take a large piece of land around typically around a block and do geological studies to evaluate for similar type prospects that we have on our block, but also for deeper and different type of deposits that potentially could be a lot larger.

Bill: And the second blue sky potential that you have brought to my attention in our first call and that this key shareholder brought to my attention was your Derecik oil exploration project in Southern Turkey. Before I share what he said, could you walk us through, what gets you excited about this project?

Art: Yeah. Okay. So part of Turkey has a little it juts down into the northern Iraq geological province, and that’s where the Zagros-basin occurs or part of the Zagros-basin occurs. And in that basin, you have the huge fields. So you’ll have 300 million barrels recoverable, a hundred million barrels recoverable, 50 million barrels recoverable, a billion barrels, production of a hundred thousand barrels per day. And it’s just progressed the flat to more of the rolling hills where they had the control and is moving north.

And that was fairly close to our block. We have the same geology. We have the same reservoirs, the same source rocks. We have oil seeps that the oil has been tested, which is identical to the oil that’s produced in the northern Iraq. And we have a location there that’s defined by seismic. We own a hundred percent. We have a large landholding and we are drill ready. And it’s an exploration location and if we hit even a small field compared to what we see south of the border, our shares are multiples of $10 value, right? Because you’re talking 50 million barrels recoverable, a hundred million barrels recoverable, a hundred million barrels we’ll have a market cap value, basically of $4 to $5 billion.

Bill: And our market cap is 20 million today just to put things in perspective. So that was why he was getting excited. And he was pointing out to me some discoveries that occurred south of the Turkey border right there in not as good of a jurisdiction that received billions of dollars of market cap that was added because of their oil discoveries. Talk to us about the benefit of being north of the Turkey border versus south in northern Iraq, where things are much more unstable and less economically favorable for the companies working there.

Art: The two issues, one is fiscal. We pay 12 and a half percent royalty and a 20% corporate tax. If we were to find say a 50 million barrel field on our side, if you cross the border, you would need about 150 to 200 million barrel field. That’s how different the fiscal regimes are. There’s a back-in clause and other factors as high royalties. That alone makes a big difference. And then also for security we’re in Turkey, Turkey is a EU country and we have a very secure area and that’s why we can drill a well for $10 million whereas south of the border. You’re talking a lot of multiples for that cost.

Bill: And that cost to drill it would be $10 million and the timeframe, isn’t it next year, 2022, where you want to test that?

Art: Yeah, we have two right now we have an extension due to COVID. And so we would really have to drill the well in 2022.

Bill: And that’s where you have referred to the SASB project as the engine, that’s the cashflow engine. That’s going to allow you to further explore, not just the SASB field in the surrounding licenses, but to pursue this Derecik License here in this potentially multi-billion dollar exploration play.

Art: Yeah, that’s correct. I just think too many companies that I call the shot in the dark. They build their whole company on a really high risk, but potentially high return project or prospect. But like you say, I have a PhD, a lot of experience, and it’s a 10% chance. It’s a good 10%, but you can’t secure a company on that. If we’re successful, we have a very high value for the shares. If we’re not, we get the write it off our income. It affects the company, not at all. And that money is generated from SASB and there’s other opportunities like this in this area that we can use SASB to generate the cash, give us stability, give us a nice growth for our shares. And then we have these high impact exploration prospects.